The Australian department store sector has been playing its own version of “sliding doors” in recent years.

The Australian department store sector has been playing its own version of “sliding doors” in recent years.

At various points in time, David Jones, Myer and their discount cousins, Target, Big W and Kmart, have all been heroes or villains in their sector.

Unfortunately, in an age of digital disruption and with the arrival of the large global retail chains, it is becoming much harder to find the “heroes” in the department compartment.

Since the GFC in 2009, Australian department store revenue has contracted by 1.8 per cent annually and experts predict only marginal increases over the next five years (0.4 per cent compound growth annually).

Consumer attitudes towards department stores tell a similarly ominous story – a recent survey by Canstar Blue revealed more than a quarter of shoppers feel they no longer need to visit brick-and-mortar department stores.

While the cards seem to be stacked against the department store format, their extinction is not set in stone, as some famous department stores are successfully evolving their models.

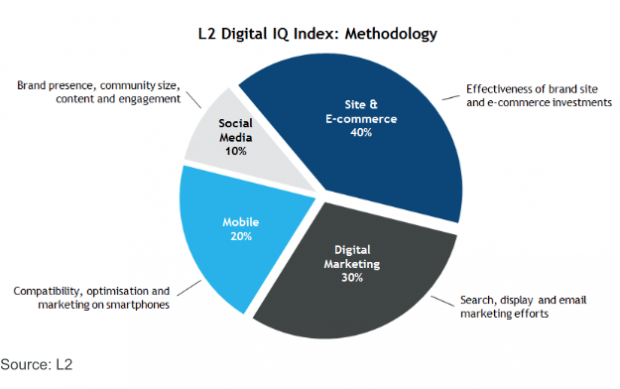

A report by L2, a US based retail think tank, suggests that the success of department store brands is inextricably linked to digital competence. L2 have developed a ‘Digital IQ Index’ to assess the tech-savviness of global department stores which they believe equates to shareholder value.

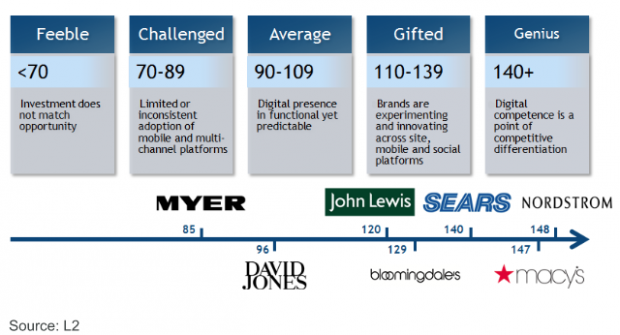

According to the L2 index, Nordstrom’s significant investment in its digital platform has paid off. With online sales now representing 25 per cent of total sales, they were crowned ‘Geniuses’ with an IQ of 148, setting itself apart from competitors by offering free shipping “No minimums. No kidding” in the States. Runners-up include Macy’s (147) and Sears (140).

Where do David Jones and Myer rank?

In the L2 Index, David Jones (96) is considered ‘Average’ while Myer (85) is ‘Challenged’. These results come as no surprise. For example, Myer’s gift registry is not linked to its online store – shoppers need to print gift details and physically purchase in-store.

Mobile-commerce has the biggest potential to reach consumers. In the epic “app vs website” debate, department stores with higher digital IQ’s have invested in both platforms. The majority of iOS apps offer social sharing, e-commerce and push notifications but less than half offer ratings & reviews, coupons and bar code scanners.

Mobile-commerce has the biggest potential to reach consumers. In the epic “app vs website” debate, department stores with higher digital IQ’s have invested in both platforms. The majority of iOS apps offer social sharing, e-commerce and push notifications but less than half offer ratings & reviews, coupons and bar code scanners.

This indicates that while department stores are on the right track, they are not quite hitting the mark. L2 reports that tablet optimised sites are the greatest missed opportunity.

Search engine visibility is the real test of a digital IQ. Some department stores are purchasing paid ads to increase their visibility and brand, while other department stores already have strong organic visibility, appearing on the first page of Google results.

Recent media reports suggest that the implementation of Google’s “mobilegeddon” is likely to lead to the ‘disappearance’ of retailers from Google if they do not have mobile enabled websites, reinforcing that this should be an area of considerable focus for challenged contenders.

Despite the sub-par ratings, Australian department stores are making in-roads to better their digital footprint.

Myer reported strong online sales growth in its recent results announcement and highlighted its intention to build “digital capability off the back of the Myer One loyalty program to accelerate omni-channel.” In addition, DJ’s new CEO, Iain Nairn, has commenced the implementation of a fresh approach with a digital focus, suggesting the current DJ systems are archaic. He plans to introduce the same retail systems that Country Road and Woolworths in South Africa successfully use.

As the digital world keeps expanding, both Myer and David Jones need to be on their A game to maintain relevant and viable businesses. The most successful international department stores have invested heavily in mobile online platforms, adopting digital competence to the department compartment.