The rapidly expanding UK sporting goods heavyweight, JD Sports, is taking aim at the Australian market following its acquisition of Hilton Seskin’s Next Athleisure.

The rapidly expanding UK sporting goods heavyweight, JD Sports, is taking aim at the Australian market following its acquisition of Hilton Seskin’s Next Athleisure.

The stronghold that local sporting goods retailers have on the concentrated Australian market is set for a challenge after UK heavyweight, JD Sports, signalled its intent to enter the Australian market by acquiring Next Athleisure.

Last week, the UK sports retailer confirmed in its half-year report that it had acquired, via its newly incorporated subsidiary, JD Sports Fashion Holdings Australia Pty, an 80 per cent stake in Next Athleisure, which operates 32 fashion stores and an e-commerce channel under the Glue Store and Super Glue retail banners. Next Athleisure also holds the franchise rights for Topshop Topman in Australia, and also owns wholesale business, Trend Imports.

Brian Small, chief financial officer of JD Sports, told Inside Retail Weekly that the group’s purpose is to use Next Athleisure’s infrastructure and management to open JD stores in Australia.

Speaking to IRW this week, Hilton Seskin, chairman of Next Athleisure, said he had been in discussions with JD for over a year and that JD represented a fitting logistics partner who will help fuel expansion for both the Glue and JD brands.

“I’ve known JD for quite some time, and I just thought that they’d be a good fit – there’s a bit of a crossover [with Glue Store] and there’s definitely efficiencies between the businesses – the Glue Store, the wholesale division [Trend Imports] and JD Sports.

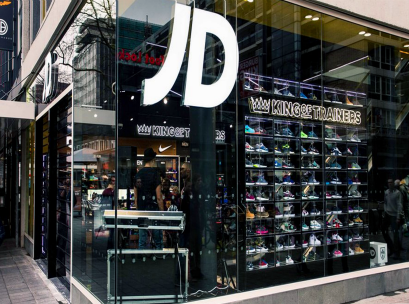

“I think that the JD offer internationally is something that is so unique to the market. Until the first JD opens [in Australia], people are probably not going to understand what that gets into. But it’s going to be bringing an offering that’s not been seen in the market.”

JD has engaged Seskin, a long-serving Australian retail veteran who founded Rebel Sport in Bankstown, Sydney in 1985, and a local team to focus on identifying and leasing prime sites for JD Sports stores, which are expected to be approximately 600sqm in size.

“It’s about the right sites, it’s about the right opportunities,” said Seskin. “It’s a brand that’s growing all over the world, so based on the opportunity, we’re not putting any limitations on the growth.”

JD Sports Fashion has been 57 per cent owned by Pentland Group since mid-2005, a group whose principal interests are in sports and fashion brands, such as Lacoste and Speedo. It operates over 840 stores across the United Kingdom, the Republic of Ireland, Germany, the Netherlands, France and Spain.

JD Sports Fashion has been 57 per cent owned by Pentland Group since mid-2005, a group whose principal interests are in sports and fashion brands, such as Lacoste and Speedo. It operates over 840 stores across the United Kingdom, the Republic of Ireland, Germany, the Netherlands, France and Spain.

In its recently reported half-year results, operating profit (before exceptional items) for the period increased by 63 per cent to £77.6 million, with total group revenue increasing by 20 per cent in the period to £970.6. It holds nearly 17 per cent of the £7.7 billion industry in the UK.

So where does JD sit within the Australian sporting goods retail market? The top four players (Super Retail Group, The Athlete’s Foot, Lorna Jane and Foot Locker) in the industry account for almost 67 per cent of revenue, indicating dominant positions in the market.

“The effect on the industry of a new UK sports brand entering Australia depends on the product range offered by JD Sports and the relative price point,” Lauren Magner, senior industry analyst, Ibisworld, told IRW. “If the company is able to provide a better offering to Australian consumers than its domestic counterparts, then it is likely this will shake up the industry.”

Indeed, providing a better offering to consumers than the established powerhouses underpins Seskin’s confidence in bringing JD to Australia, who arrive with a, “slightly different offering”.

“It’s the fashion end of sport – Rebel is core sports, then you’ve got fashion businesses; it sits in the middle,” he said. “The strength of JD will mean that the amount of new product that will come to market is going to create some market accretion, because we’re going to add to the market, which is what we want. To bring in new businesses just to cannabilise the market is not the smart thing to do, and we just see that the market is going to grow with the JD offering.”

JD to challenge Rebel Sport?

JD to challenge Rebel Sport?

With nearly identical brand colours and on the surface, similar value propositions, JD’s entry stands to have the most impact on Rebel Sport, which along with Amart Sports, gives Super Retail Group 30.4 per cent marketshare according to Ibisworld research. Though, it seems at this early stage, SRG isn’t too flummoxed about JD’s impending market entry, suggesting that more consumer choice is a good thing for the market.

“We see plenty of potential for continued growth in sports retailing in Australia, an SRG spokesperson told IRW. “At a macro level, revenues are expected to continue to benefit from a greater focus on healthier, more active lifestyles, and the continued strong performance from our Rebel and Amart Sports business is reflective of that.

“The Australian market remains relatively fragmented, and, speaking to our own business, we still see significant potential to bring to bear our scale and maturity, and the advantages that offers in terms of our deep local knowledge, supply chain, capital resources and marketing, to continue to grow and strengthen our national network.”

While what JD introduces may be a slightly different offer, prospective entrants that do not have a specific market, but seek to sell a range of general sports apparel and footwear need to consider the market dominance of existing players.

“The industry is highly competitive, as many chains are well established and have recognised brands,” said Magner. “These brands have taken many years to establish, often at great marketing and relationship-building cost.”

Historically speaking, the majority of fitness and athletic clothing stores have been small, family-run businesses operating in local areas. However, the benefits of bulk purchasing, a nationally recognised brand and other synergies, have allowed Rebel and Amart Sports, The Athlete’s Foot, Lorna Jane, Foot Locker and other company-owned chains to gain a dominant foothold in the industry, which has affected the viability of smaller operators.

“The expansion model of these mass merchandisers has been to open new stores rather than to acquire existing retailers operating in the industry, meaning individually owned businesses have been forced out in some areas,” said Magner.

SRG also believes its, “long and supportive relationships with the world’s best sporting brands and Australia’s sporting bodies” are a major competitive advantage.

But perhaps JD, off the back of strong performance across Europe, is confident that there’s more of the Aussie sporting goods pie to be had, given the fitness and athletic clothing stores industry has flourished over the past five years in spite of the volatile retail market. Changing consumer attitudes and trends have led to the prevalence of activewear as streetwear, with Ibisworld expecting industry revenue to grow over the next five years, rising by an annualised 2.9 per cent to reach $2.3 billion in 2021-22.

So, will JD pose a legitimate threat to Rebel’s stronghold in Aussie sporting goods retail?

Given that industry participants compete based on price, product range, marketing, size of operations and reputation, JD may need to pinpoint a different calling card in order to establish a foothold and impress Aussie consumers.

“One of the main ways the industry competes is through service,” said Magner. “Stores like The Athlete’s Foot and Rebel train staff to ensure they have a high degree of product knowledge and can provide expert recommendations to customers. These services provide a competitive advantage and encourage customer loyalty.

“If JD is able to provide high levels of customer service and opens store locations in popular areas, it is expected that this will place some pressure on Rebel’s performance.”