Contactless payment methods will all but replace traditional physical credit and debit card payments by 2020 for transactions under $100, according to business information analyst, IbisWorld.

Contactless payment methods will all but replace traditional physical credit and debit card payments by 2020 for transactions under $100, according to business information analyst, IbisWorld.

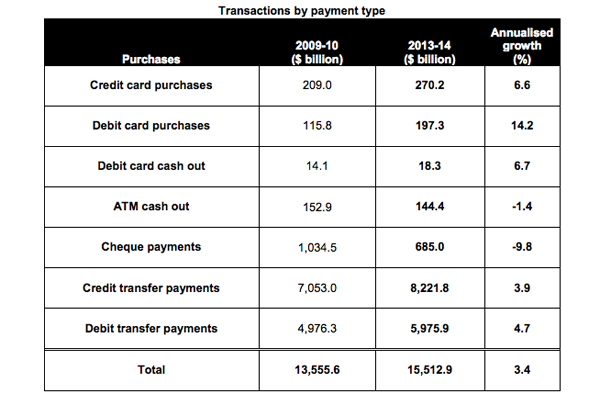

Overall, PIN-only and contactless credit card and debit card purchases are likely to continue their assault on cheque and cash options, after posting annualised transaction growth of 6.6 per cent and 14.2 per cent respectively over the four years through 2013-14.

“With the increase in online shopping, credit and debit transactions will continue to dominate the payments system for personal use and carve an increasing piece out of ATM withdrawals, despite holes in the wall being in more locations than ever before,” IbisWorld Australia GM, Dan Ruthven, said.

“In the coming years, contactless payments and paying using a mobile phone will begin to replace the standardised plastic cards we’ve widely used since the 1980s,” said Ruthven.

IbisWorld expects the big four retail banks to retain their dominance of the lending market.

The big four controlled some $2.3 trillion of loans as at June 2014 – significantly more than the $87.9 billion of outstanding loans provided to households and businesses by financial corporations other than the banks.

“While banks remain the dominant force behind consumer and business lending, Coles’ impending foray into personal loans could be indicative of things to come as supermarkets, airlines, and department stores attempt to muscle in on the market.”

IbisWorld has identified a decline in barriers to entry as one of the main driving forces behind the increase in non- traditional banking.

Companies that operate across multiple sectors can provide financial lending products if certain criteria are met – specifically, becoming an authorised deposit-taking institution and obtaining a licence from the Australian

“There’s little standing in the way of non-traditional firms entering the retail banking sector,” said Ruthven.

“Improving technology, centralised contact points, and the reduced use of branches are the main factors driving new companies into the uncharted waters of retail banking.”

Cementing customer loyalty, product innovation and diversification, and developing new revenue streams are the key incentives driving non-traditional players towards banking, insurance and other financial services.

“Australian supermarkets and other non-traditional providers are streets behind their British counterparts, with Sainsbury’s Bank and Tesco Bank both being set up in 1997 against a backdrop of liberalised regulation.”

However, until employers start paying wages to accounts other than those provided by the major banks and until the mortgage industry becomes decentralised, it will be difficult for new financial providers to significantly erode the marketshare of the established big four and for emerging payment systems to carry increasing capital flows.

The number of bank, credit union, and building society branches fell by 130 during 2012-13, continuing a long-term decline and resulting in one branch for every 3,558 Australians. In the five years through 2019-20, IbisWorld expects the numberof people per branch to increase to 3,847.

“The decline in bank branches has been most rapid in regional areas, in line with lower population density and reduced demand for in-branch services due to the greater accessibility of online platforms.”